Robo investing sounds like a complex investment option, but it is actually very simple. It involves selecting the best investment options based on your needs like the returns you anticipate. Robo advisors use computer algorithms to advise Robo investors on the best investment portfolios and investment management. Well-known examples of leading robo-advisor companies are Schwab, Betterment, Ellevest and Wealthfront. How to Choose Robo Advisors ?

What is Robo Advisors Investing?

Robo investing is investing using computer algorithms to get financial advice or investment management. It’s an automated process. Robo advisors are online platforms that use a computer algorithm to provide financial planning based on investor’s needs. Robo advisors require little to no human supervision to build and manage an investment portfolio. Robo advisors are cheap and help Robo investors automatically select good investments with long-term returns.

What is a Robo Advisor?

- A Robo Advisor is an automated computer algorithm that provides financial advice and investment portfolios based on the investor’s needs. It requires little to no human supervision.

- Robo advisors collect information from you the investor and then use the data to find the best investment option for you. When choosing a Robo advisor, compare management fees, account type, and services offered by different Robo advisors.

What is a Robo Investor?

A Robo investor is a person who uses digital platforms that use a computer algorithm to select the best investment option based on his or her needs like risks appetite and returns.

How Robo Advisors Work

Robo advisors collect information from clients through online surveys. Once they have collected the data, they use computer algorithms to provide the best financial advice to investors. They perform handle complex tasks like automatic rebalancing and tax optimization. Other services offered by Robo advisors include goal planning, account services, customer service and portfolio management.

Robo advisors use factors like risk appetite, amount of returns you want and the time you want the returns to select the best investment for you.

Main Reasons to Use a Robo-Advisors

Thousands of people are turning to robo-advisors. That’s partly because it’s so easy to start investing with them. Some of the other reasons investors use robo-advisors include: transparent and low fees, having a Diversified portfolio and them being tax efficient.

- Easy to start. The process of investing with a robo-advisor is relatively easy. All you have to do is register for an account, deposit money, answer a few questions, and the robo-advisor will do the rest.

- Transparent fees. Unlike other financial advisors, robo-advisors have transparent pricing.

- Low fees. The robo-advising industry is relatively competitive. This has led to the industry having some of the lowest fees in the industry.

- Experienced experts. Most robo-advisors employ some of the most experienced professionals.

- Diversified portfolio. Robo-advisors help create a quality portfolio based on your risk appetite.

- Tax efficient. These advisors use the concept of tax-loss harvesting to minimize the amount of taxes you have to pay.

How to Choose Robo Advisors

When looking for the best Robo advisor, compare fees and features between different Robo advisors. Also, compare services offered and the availability of human advisors. Select one that is offering the best services and charges low fees. When selecting the best Robo advisors, you want to consider factors such as management fees, account type, services offered and the support you get.

- Management fees. You need to compare fees between different Robo advisors and weigh them against the features and benefits you will be getting.

- Account type. There are two types of Robo advisors accounts; Retirement Accounts and Taxable Accounts. Retirement accounts have tax advantages and they include IRAs and 401k(s) and Taxable Accounts that do not have any tax advantages.

- Services offered. Compare services offered by various Robo advisors. For instance, most Robo advisors are now offering tax-loss harvesting and automatic re-balance without additional cost.

The Best Robo-Advisors

To get long-term returns, you need to select the best Robo advisors in the market. The following are some of the top Robo advisors you can consider. They include Betterment, WealthFront, Schwab, Ellevest and Ally Invest. Other good Robo Advisor Companies options are listed following our comparison.

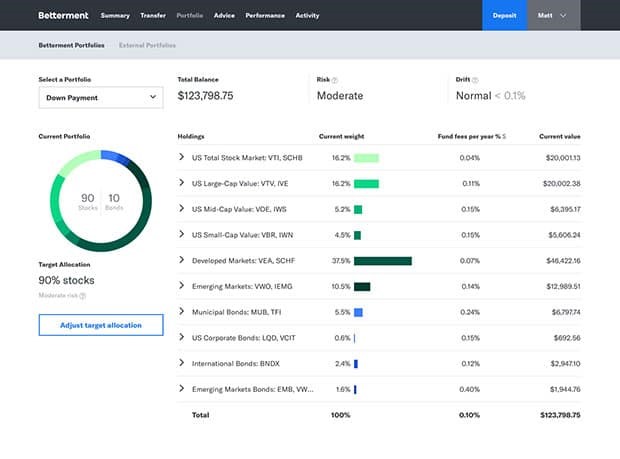

1. Betterment Robo-Advisors

Betterment is among the pioneers of investment using Robo advisors approach. Betterment Robo advisors was started in 2008 and has more than $16.4 billion in assets under management. The company has raised more than $275 million from investors like Menlo Ventures. It is now valued at more than $1 billion and has more than 400k customers.

How Betterment Works

Betterment works in a very simple process. After creating an account, the company will ask you a number of questions about you. Some of the questions are about what you are saving for and when you expect to hold the investment. The company will then build an intelligent portfolio that includes bonds, stocks, and ETFs. Further, the company’s financial advisors will help you decide how much money to invest. Other features are: Smart rebalancing, Auto-depositing, Reinvesting dividends, Tax-loss harvesting.

Betterment Fees

An important thing with Betterment – and other robo-advisors – is on the amount of fees they charge. With Betterment, you pay an annual fee of 0.25% on every $1,000 invested. For a premium account of more than $100k, you pay 0.40%.

2. WealthFront Robo Advisor

Wealthfront is one the best robo-advisors in the US. It was started in 2008 and has more than $11.4 billion. The company has raised more than $204 million from venture firms like Tiger Global Management and Spark Capital. Wealthfront has a valuation of more than $500 million.

How Wealthfront Works

Like Betterment, all you need to do is to create a free account on the website or Wealthfront app, answer a few questions, and the company’s algorithms will select the investments. The company’s main features are: Tax-loss harvesting, Stock-level tax loss harvesting, Smart beta, Risk parity, Portfolio line of credit with low interest rates.

Wealthfront Fees

Low fees is one thing that makes Wealthfront a viable investment platform. The company charges you a low 0.25% advisory fee. In addition to this, you pay an expense ratio of between 0.07 and 0.16%. This is a fee that money management companies charge to run the funds.

3. Schwab Intelligent Portfolios

Schwab Intelligent Portfolios is a robo-advisor arm of the giant brokerage company, Charles Schwab. The product was created in 2015 and has grown to amass more than $37 billion in assets under management. It has more than 300k accounts.

How Schwab Intelligent Portfolios Work

Like with Betterment and Wealthfront, Schwab Intelligent Portfolios work in a simple way. All you have to do is create an account, answer a few questions, and the algorithms will take over. In addition, you earn interest on your cash.

With Schwab, there are no advisory fees and no commissions. The company makes money through ETFs that Schwab has created. In addition, part of your funds are invested in a FDIC-insured account. These funds earn interest, which the company earns. It also makes money from the order flow.

4. Ellevest Robo Advisor

Ellevest is a robo-advisor that was started in 2014. While the company works in a similar way to the above three, it distinguishes itself by focusing mostly on women. In fact, most of the company’s employees are women. The company has raised more than $77.6 million from the likes of Melinda Gates and Morningstar. The company has more than $280 million.

How Ellevest Works

Ellevest has three products. Ellevest Digital is an easy online investing tool that uses algorithms tailored to your salary, gender, and lifespan. There are no minimums. The Ellevest Premium offers all services offered in Ellevest Digital, plus one-on-one career coaching and financial planning with people with $50k or more. Finally, the Private Wealth product offers all the other products for people with more than $1 million. To invest, all you need to do is create an account, answer a few questions, and the algorithms will do the work for you.

Ellevest fees are based on the product you have invested. For Ellevest Digital, you pay 0.25% annual management fee while for the Ellevest Premium, you pay a management fee of 0.50%.

5. Ally Invest

Ally Invest is an arm of Ally Financial, which is a leading online bank that is valued at more than $13 billion. Ally Invest has more than $4.7 billion in assets under management and more than 260k customers.

How Ally Invest Works

Like in other robo-advisors, the company works in a simple way. You just create an account, tell it about your financial goals, and then the company will recommend to you a diverse mix of ETFs. Ally charges a small fee of 0.30% a year.

Ally Invest crypto: Can you buy bitcoin on Ally Invest? Unlike other investment platforms such as Robinhood, you can not buy cryptocurrency on Ally Invest

Other Good Robo Advisor Companies

While these are the leading robo-advising companies, there are others that you can chose from. Some of the most popular ones are:

- Lending Club. It is a Peer-to-peer lending company but it has an automated product.

- Prosper. It is similar to Lending Club

- Acorns. Acorns allows you to invest your spare change. It is one of the best robo advisors for new investors.

- Vanguard Personal Advisor Services. This is offered by Vanguard, the biggest asset manager in the world.

- Fidelity Go. Offered by Fidelity, one of the biggest broker-dealers in the US.

- TD Ameritrade Essential Portfolios. Offered by TD Ameritrade Bank.

- SoFi Invest.

- Stash

Robo-advisor Comparison Conclusions

Robo-investing is a relatively new way to invest your money, especially if you don’t have the skills or the time to pick your own assets. To maximize your returns and avoid risk, it is recommended that you invest in two or more robo-advisors.

It is also recommended that you invest in other diversified assets like index funds, mutual funds, and ETFs. Using our comparison of robo advisors, you will be in a better position to choose the best robo advisor for you.