Peer to peer investing sites can be a good way to diversify your portfolio or even to get started with investing. Peer to peer lending returns can be enormous. What are some of the best p2p lending for investors in 2023, and what are the risks?

Growth of peer to peer lending business

- Recently, the peer to peer lending industry has seen impressive growth. According to studies, the industry is expected to have a CAGR of 25% until 2025, when it will reach more than $850 billion.

- The industry is currently dominated by companies like Prosper, Upstart, Funding Circle, Mintos and Bondora. It is to no surprise that these platforms are among the best peer to peer lending companies for investing.

- Borrowers are using p2p lending sites and apps mostly for personal loans, real estate financing and business loans.

Peer to Peer Lending Platforms

The Peer to Peer Lending industry is currently dominated by platforms like Prosper, Upstart, Funding Circle, Mintos and Bondora. You can find our reviews below.

Prosper Marketplace

Prosper lending has achieved a lot of success in the past few years. Since inception, the company has given out loans worth more than $14 billion.

To invest in the Prosper marketplace, all you need to do is to sign up, explore the borrowers who are listed, invest in the customers or let the system do it for you, and then earn the returns as the customers pay back the cash. As an investor, you should invest in Prosper because of its proven track record in the industry, its returns, which average about 5.3% annually. In addition, peer to peer lending with Prosper is simple and straightforward.

4 Reasons why you should consider Prosper Marketplace

- The second biggest peer-to-peer lending company in the US.

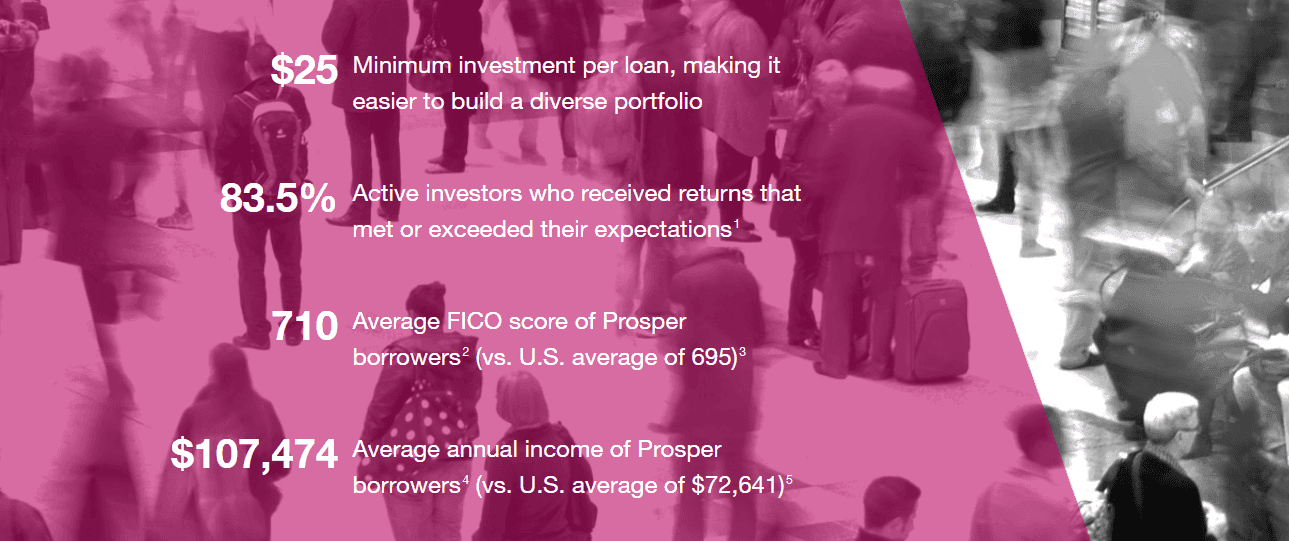

- A well-known brand with great customer reviews. 85% of its customers have received returns that have exceeded their expectations.

- Easy to get started. You can start with as little as $25.

- Quality borrowers with an average annual income of more than $107K.

Upstart: Funding the under-banked

In the United States, there are other peer-to-peer marketplaces that you can invest in. For example, Upstart, which was established in 2014 has already offered loans worth billions of dollars. The key difference between Upstart on the one hand and Prosper on the other is that it targets fresh graduates, who don’t have the required credit score.

The company has developed its own criteria of evaluating the creditworthiness of the customers. As a result, the returns tend to be higher – and risky – than those of the other peers. The chart above shows a summary of the company’s loans.

Key benefits of investing in Upstart:

- Higher returns than other p2p platforms.

- Easy to start investing.

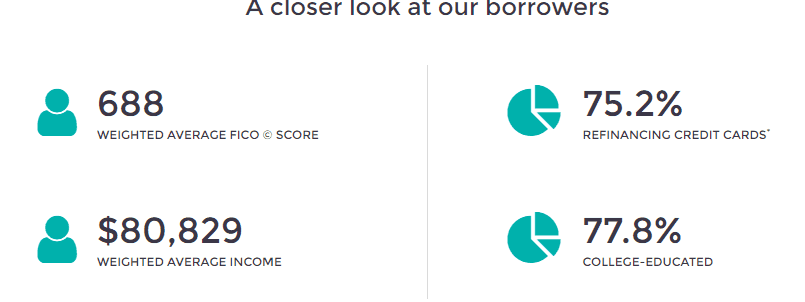

- Average annual income of borrowers is more than $80,000.

- Automated investing capability.

Funding Circle: Business Loans

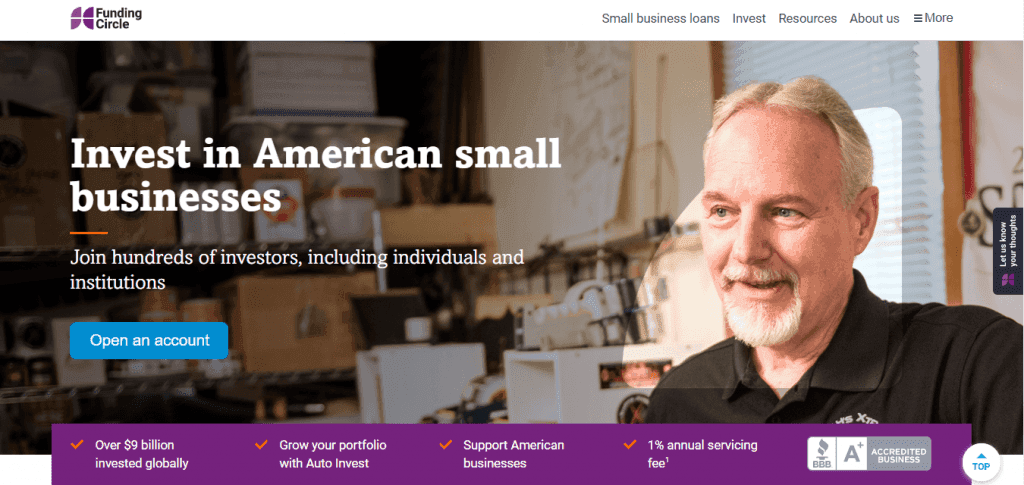

Unlike Prosper and LendingClub, Funding Circle specializes on business loans. Over the years, the company has invested more than $9 billion in companies from around the world. It has more than 85K investors, who include individuals, national banks, and governments.

Like with the previous platforms, all you need to do is to create an account, fund it, analyze investments, and make the investments. To do so, the company accepts a minimum of $25K and to promote diversification, only 2% if the total funds can be invested in one note.

4 Reasons why you might want to consider using Funding Circle:

- One of the biggest P2P companies in the world.

- It is an easy process to invest.

- It only invests in companies, making defaulting a bit hard.

- It handles everything for you if a business is unable to fully repay their loan.

- Use of rigorous technologies to assess risks.

- Transparent pricing of just 1%.

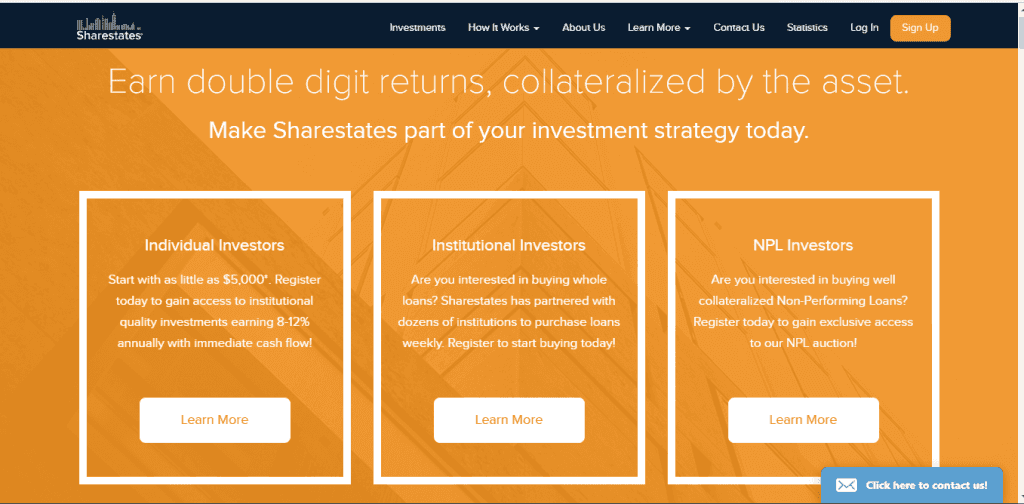

Sharestates is a totally different peer-to-peer lending marketplace because it targets only accredited investors and institutional investors. The company gives these investors access to a marketplace that is made up of mostly real estate professionals. To reduce risks on the investments, the company has developed a 34-point underwriting process that has proven to be effective over the years. Individual investors are required to start investing with as little as $5000.

Benefits of investing using Sharestates

- It is a simple process that takes less than a day to complete.

- An ideal way to invest in real estate.

- Access to investing in collateralized non-performing loans.

- High yields of between 8% and 12%.

- Relatively safe investments.

Bondora Go&Grow

Bondora is an Estonian peer to peer lending site, that offers a 6.75% interest rate combined with the possibility to immediately take out your money for a fee of only 1 euro. If you’re outside Europe and you want some exposure to the Euro this can be a good way to earn a nice yield simultaneously.

More lending platforms for investors. Other than these P2P lending platforms in the US, there are other types of alternative lending platforms. For example, there are companies like Microventures, Kickstarter, and CircleUp that allows you to invest in small startup companies. Furthermore, new lending platforms pop up regularly. Outside the United States, you may find even higher returns.

How Peer to Peer Lending Investing works

The industry works in a basic way. In the marketplace, people and companies in need of peer to peer loans can apply and get it in a short timeframe. On the other hand, investors, who require yield, can deposit money in these companies and then lend to these people. Peer to peer lending platforms like generate their profits by taking a cut of the interest rates paid by the borrowers.

Risk profile

Generally, when it comes to peer to peer lending risks, the higher the potential yield, the higher the risk. P2P lending is most similar to investing in bonds. Given that some bonds are already giving negative yield, you may consider some P2P loans with interest of 10% a bit like junk bonds, given the much higher interest rate.

The advantage of investing in P2P loans is that you can count on a nice cashflow. The downside is that if the economy tanks, many borrowers will not be able to pay back their loans and an investment portfolio that mostly consists of P2P loans will do terribly in this situation. For this reason, we don’t recommend investing more than 10% of your net worth in P2P loans.

Advantages

P2P lending can provide a steady source of passive income, offers easy diversification opportunities, and tends to have a low correlation with stock markets and interest rates.

Disadvantages

P2P portfolios can be vulnerable to significant declines in value during economic shifts, and U.S. investors may encounter complexities when integrating P2P investments into tax-advantaged accounts.

Peer-to-Peer Lending’s Popularity in the United States

After the 2008/2009 financial crisis, many Americans grew disillusioned with the traditional financial system. The perception of taxpayers bailing out big banks like Goldman Sachs and Morgan Stanley left a bitter taste. In response, they sought alternatives in the lending industry.

One such alternative is peer-to-peer lending, which has streamlined the loan application process. With just a few simple steps that can be completed using a smartphone, it offers convenience and accessibility.

Furthermore, peer-to-peer lending platforms often provide credit at lower rates compared to traditional banks and credit cards. Their online-only nature allows them to operate with reduced overhead costs, translating into more affordable lending options for consumers.

Borrowers are using p2p lending sites and apps mostly for personal loans, real estate financing and business loans.

Peer to Peer Lending Returns

For investors, the peer to peer lending marketplaces provides them with an alternative avenue to make money. This is because the industry has become a separate asset class in itself, which allows investors – individuals and institutions – to lend money to customers and make good returns on their investments in peer to peer loans.

In addition, the companies in the industry have created specialized peer to peer algorithms that help to detect a customer’s credit rating and their chances for defaulting.

Finally, for investors, the platforms are easy methods of investing their money. As with borrowing, all an investor needs to do is to deposit funds and then lend. Some platforms like Bondora have peer to peer algorithms that can automate the process and to automatically find the best peer to peer investment to optimize your returns.

Takeaway: Focus on the Established Platforms

Investors seeking diversification and attractive returns can consider peer-to-peer lending platforms as part of their investment strategy. While numerous platforms emerge regularly, it’s advisable to concentrate on established ones, as discussed in this article. Investing in these reputable companies offers the benefits of diversification, potentially high returns, and the satisfaction of earning passive income. After gaining insights into the peer-to-peer lending market, you may wonder whether it’s the right investment for you. Here are some considerations:

- Long-Term Investing: If you’re planning to invest for a period of 20 years or more and are comfortable with a buy-and-hold strategy, broad index funds may offer better returns over time compared to the peer-to-peer lending space.

- Emotional Resilience: If market fluctuations make you nervous, peer-to-peer lending can be a less stressful alternative.

- Alternative Approach: Another approach involves keeping most of your funds in cash and allocating a small portion, around 1%, to investments like Bitcoin, rebalancing when Bitcoin experiences significant gains. This strategy has historically proven effective and risk-averse. Additionally, considering cash flow-generating assets like peer-to-peer loans or real estate can be prudent even within this approach.